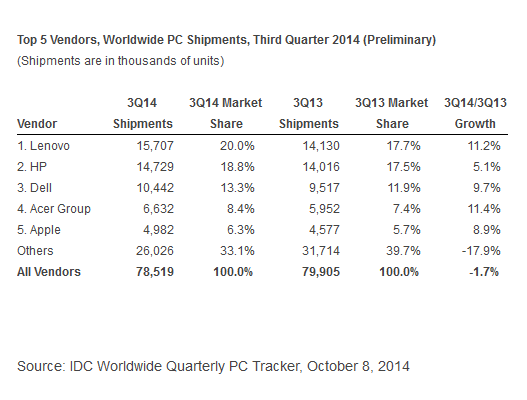

Framingham, Mass. — Worldwide PC shipments dropped 1.7 percent to 78.5 million units in the third quarter, marking a sizable improvement over prior forecasts for a 4.1 percent category unit decline, according to IDC Research quarterly PC tracker results.

“Moving forward, we expect a healthy holiday season, hence the U.S. PC market may maintain a positive growth rate. However, low demand for large commercial refreshes, combined with competition from 2-in-1 systems, may limit the growth potential,” stated Rajani Singh, IDC personal computing senior research analyst.

IDC said many of the trends from the second quarter continued in the third-quarter, with commercial PC purchases playing a key role in many markets.

The top three vendors – Lenovo, HP, and Dell – all showed solid year-on-year growth, the report said.

At the same time, fierce competition and a spiral toward tablet-like prices led to further market consolidation.

Shipments of entry systems, including Chromebooks, continued to inject an important source of volume and sustained improved consumer demand in certain markets over recent quarters, IDC said.

On a geographic basis, IDC said mature markets including North America and Europe continue to drive the market, and showed “significant improvements across segments.”

As Windows XP migrations have slowed, the firm said, an improved business outlook, tablet saturation in some markets, and expanded offerings of competitive notebooks played roles in the improving results.

“Although shipments did not decline as much as feared, these preliminary results still show that 3Q14 was one of the weaker calendar third quarters on record in terms of sequential growth,” cautioned Jay Chou, IDC worldwide PC trackers senior research analyst. “The third quarter has historically been driven by back-to-school sales and renewed business purchasing, which were weaker than normal this year.”

He continued that “the current growth of lower-priced systems, while encouraging in the short run, brings concern for the long-term viability of vendors to adequately remain in the PC space.”

Singh said “PC shipment growth in the United States remained slightly faster than most other regions in the third quarter and overall the U.S. PC market came in right on forecast with 4.3 percent year-on-year growth.”

Singh attributed the U.S. performance to solid back-to-school sales, a strong performance from key vendors, the continued acceptance of Chromebooks, some commercial uptick from Windows XP to Windows 7 migration, and the slowdown in tablet sales.

Third quarter U.S. PC unit shipments totaled 17.3 million, as the U.S. market grew by 4.3 percent from the same quarter a year ago and 2.6 percent from the previous quarter, IDC found.

“Growth centered in strong momentum from the portables category, which grew by more than 9 percent year over year. Desktop shipments were relatively sluggish this quarter and growth remained in negative territory,” IDC said.

Among the leading global vendors was Lenovo, which maintained its lead as the top PC supplier, with another record volume number of 15.7 million units.

HP shipped 14.7 million units for No. 2 with growth surpassing 5 percent.

Dell saw shipments grow 9.7 percent to more than 10 million units, behind strong performance in notebooks in the U.S. and Asia/Pacific (excluding Japan).

Acer grew over 11 percent, in part due to low volume a year ago but also from the success of its Chromebooks and entry-level notebooks, IDC said.

Apple moved into the No. 5 position on a worldwide basis, slightly overtaking Asus. The company’s steady growth, along with recent price cuts and improved demand in mature markets, has helped it to consistently outgrow the market, according to the quarterly tracker.