Consumer electronics TV hardware pricing today has become big news in the popular press and elsewhere. Just look at some of the recent headlines:

“The cost of big-screen televisions, which has been steadily dropping by about 25 percent a year, is now expected to fall even more sharply this autumn, according to industry analysts.” — The New York Times

“Prices for flat panels have finally begun to tumble — by as much as 35 percent in the past year — as soaring demand for the two leading flat-panel technologies, plasma and liquid crystal display, or LCD, attracts a host of new competitors.” — Associated Press

“In Q2, the average selling price for a 42-inch HD plasma TV plummeted 18 percent from Q1 2005.” — Quixel Research

Yet prices aren’t the only things falling in the TV hardware business — so are many preconceived notions about how the digital revolution and new technologies would affect the TV business. If the TV business was a cruise, we’ve all been on rough waters of late and the outlook is higher seas.

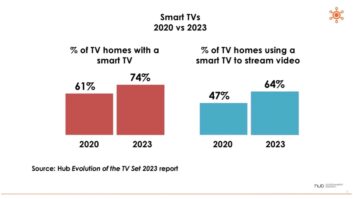

Why? First and foremost, consumers in ever-growing numbers are falling in love with flat-panel televisions. According to industry data, twice as many flat panels will be sold worldwide this year, compared with 2004, and projections show that the sky is the limit.

But what has this meant for the store floor where these televisions are sold? For starters, it has meant a realignment of product offerings which is already well underway — trending away from “bulky” CRT direct-view TVs, which don’t offer the form factor of flat panels; trending away from traditional CRT-based rear-projection TVs, which don’t have the sex appeal of flat panel or microdisplays and which no longer offer their usual major price advantage over large screen technologies; and trending heavily toward digital and high definition, away from analog.

However, the explosion of flat-panel demand has come with a strange bedfellow: accelerating price erosion. Defying conventional economic theory, the 2005 marketplace is proving to be a dysfunctional market: Demand is strong, so supplies are limited, yet pricing continues to fall.

For the dealer, this has had a drastic effect on both the top and bottom line. The cycle of flat-panel price erosion has played havoc with a retailer’s ability to meet budgetary plans.

Despite turbulent market conditions, however, many dealers have grasped the notion that accessories, such as entertainment furniture — including TV stands, entertainment centers, media storage and mounts — can go a long way toward filling their bottom lines. With renewed interest in accessories marketing, and an increasing need to have accessories sales, trade associations and media have recently focused on accessories such as furniture for electronics.

In research sponsored by the Consumer Electronics Association’s (CEA) accessories division, non-CE manufacturers and retailers such as Land Rover, Ikea, Weber and Crate & Barrel were studied to determine the best practices for accessories retailing.

The results of that research were then applied to CE environments, yielding 12 best practices for CE accessories retailers. While the full content of that report can be obtained from CEA, some of the key best-practice suggestions which apply to today’s TV marketplace are highlighted below.

Encourage physical adjacencies: Accessories should be located physically adjacent to host devices within the store, sometimes in multiple locations. In the CE world, this means floor-lining TV stands and mounts in the same environments as the televisions themselves. In this way consumers visually grasp how the products are co-dependant and are more likely to consider them a package purchase. While this seems intuitive, it is often overlooked.

Practice experiential marketing: Retailers should provide environments that replicate the entire experience as an opportunity to demonstrate the importance of accessories in completing the entire experience. In golf retailing, this means mini-indoor driving ranges to test out equipment. In consumer electronics, room vignettes serve this function to allow the consumer to experience how these CE products can actually be used at home.

Develop incentive compensation based on attach rates: Progressive, category-based compensation structure based on attachment rates should be adopted. For those dealers who still have assisted sales floors, the notion that accessories contribute greatly to the bottom line means that compensation should encourage those sales.