Worldwide CE sales were flat in 2017 vs. 2016, at $677 billion, despite pockets of growth seen in VR, voice assistants, smart home, headphones, connected car and wearables, according to research by Futuresource Consulting.

Innovation in CE is generally shifting consumer spending from one category to another as opposed to lifting overall revenues. 2018 is forecast to perform somewhat stronger than 2017 with 2 percent uplift in revenues, however longer term CE growth prospects are limited to low single-digit levels, since the mobile market is peaking and represents half of overall revenues.

Emerging markets continue to underwhelm, while the U.S. remains the leading driver of new emerging CE categories. China, the world’s largest CE market, fell percent in 2017, despite an increase in total volume demand. “It’s a harsh landscape, but there are patches of sunshine,” says Simon Bryant, associate director at Futuresource Consulting. “We’re seeing growth in some TV and A/V products, with digital media adapters/media streamers, home audio and headphones attracting much-needed consumer attention.

Mobile remains CE’s all-star player, and now delivers 50 percent of total global consumer electronics revenues, with smartphones surpassing 1.7 billion units and trade value growing 5 percent in 2017. By 2021, the global mobile category will be worth more than $420 billion.

The market decline in TV displays market has bottomed out after losing more than $37 billion in value since the peak of the flat-panel boom, only seven years ago. Consumer appetite for more expensive sets and a shift to 4K UHD will bring a reversal of fortune. Futuresource’s forecasts point to a total A/V category market value in excess of $150 billion by 2021, with TV displays accounting for most of the value growth.

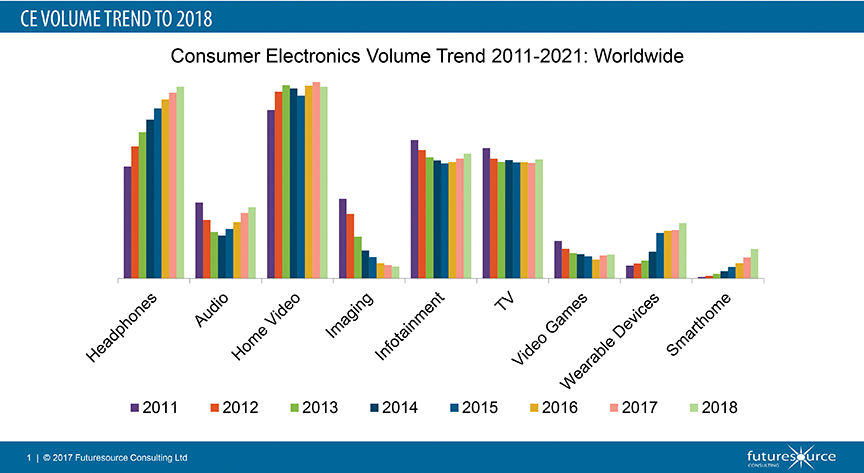

Within audio, smart speakers reached 25 million units in 2017 and boosted overall audio volume, while a portion of the market cannibalized Bluetooth speaker sales, particularly within the U.S. and U.K.

Although the virtual reality market grew in 2017, the rate of consumer uptake continued to disappoint following a muted performance during the preceding twelve months. Many factors have conspired to limit widespread adoption of VR notably high hardware pricing for PC-based VR and to a lesser extent PSVR.

Smart home continues to develop, with fragmentation and lack of interoperability across rival ecosystems becoming less of a concern, thanks in part to the anticipated success of voice assistants as a natural interface for the smart home. Integration between devices and connectivity protocols are establishing themselves and paving the way for whole-home ecosystems. Although the category will only contribute a small slice to overall CE revenues, it is an attractive new battleground which presents an additional revenue stream for brands, OEMs and service providers alike.

After a promising start, the wearables sector has since stalled however there’s plenty of life left in the category and next year we’ll see a turnaround. Look out for devices that differentiate themselves from mobile, particularly in the smartwatch category, and marketing messages that accentuate the differences and tap into the mainstream. Our forecasts show strong wearables growth out to 2021 and beyond, with a CAGR of 22 percent.

Automotive infotainment grew to account for nearly 5 percent of total CE value, passing $30 billion with robust growth of 4-5 percent expected to continue for the next 5 years at least.

Autonomous vehicles will boost the in car entertainment market, and will reach consumer markets by 2020/2021, with production of level-4 vehicles rising to approximately 10 percent of all vehicles by 2035.

Looking at the bigger picture, on a worldwide scale CE market growth is beginning to reach an equilibrium. Previous deterioration in developed markets has been reversed, but the recent growth in emerging markets is on a slowdown, despite a few pockets of sector growth.

“In September China received its second credit rating downgrade of the year,” said Simon Bryant, associate director of consumer electronics at Futuresource. “This reveals the extent of current economic difficulties, amid fears that rising debts are adding to economic and financial risks. There’s no doubt that this turbulence will continue to influence the global CE game. Now, more than ever before, the outlook for companies operating in this arena will be determined by the strength of their business planning. The strategic decisions they make, both on a category level and by bringing geographical opportunities into hard focus are central to survival and will define their future success or failure.

“Over the next five years, Futuresource expects an array of new categories to emerge in the CE landscape, including robots for care, domestic assistance and infotainment purposes, as well as innovations within the smart products category.

“Watch out for a new wave of hybrid smart products, hinted at by the capabilities of Sony’s Xperia Touch, which has the potential to be a multi-purpose home hub, acting as the primary interface for many applications,” said Bryant. “The future CE landscape does look challenging, but for the right company with the right approach, the opportunities could be boundless.”