Keeping up with the Joneses — much less keeping ahead — is an ongoing challenge for all consumer technology companies. If you’re going to establish yourself as a leader in, or simply take advantage of, a hot new product category, you have to “go big or go home.”

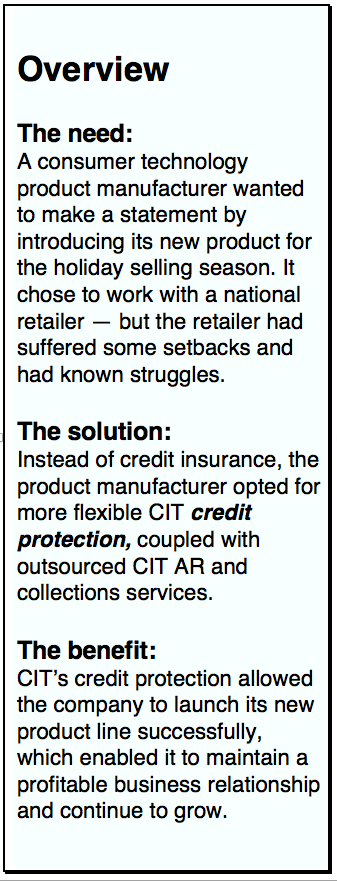

For instance, a consumer electronics accessory manufacturer decides to enter the fitness tracker market by creating a new, independent division, they turned to one of their preferred, long-time national retailers to help them make a big holiday season, market-entry splash. The accessory company and the retailer agreed on a $5-million order of their new fitness products — enough to cover Black Friday promotions through the holiday season and part of Q1.

The large size of the order made the vendor uncomfortable in assuming this much credit risk without credit coverage. Considering the size of the order, coupled with the importance of the product and division launch, the manufacturer naturally wanted to protect itself against such a large financial exposure.

There was another good reason for the company’s logical caution: Like many brick-and-mortar outlets, the national retailer involved had suffered some setbacks and its long-term turn-around plans were a frequent subject of business press speculation.

Because of these financial concerns, the retailer’s credit insurers declined to protect such a large order, leaving both the retailer and the vendor struggling to complete the sale. To salvage the order and the launch, the retailer advised manufacturer of the fitness tracker to contact another of its long-time business relationships — CIT Commercial Services.

Difficult situations like this occur in the retail market all the time, and it’s not uncommon for credit changes to occur (both up and down) during the life of a relationship. “Credit is a living, breathing thing” observes Niraj Lal, business development officer with CIT Commercial Services. “It changes based on many criteria. If a retailer performs well and grows, it typically needs more and more credit to fuel its growth. Conversely, when a retailer struggles, its reliance on trade credit becomes even more important.”

“We have had a long and deep relationship with the retail trade,” says Lal. “Open communication is a crucial part of that relationship. That open communication and confidence in the retailer’s management allowed CIT to continue to support the company.”

Credit Protection Advantages

The credit protection that CIT Commercial Services provides is not credit insurance; however, for many companies, it’s truly a much better alternative. Essentially, as one of the nation’s largest commercial factors, CIT assumes credit risk on accounts receivables that it purchases.There is typically no deduction or co-pay involved in the credit protection available with factoring products. Also, unlike a credit insurer’s hefty, prepaid, flat premium, CIT’s fees for its credit protection services are based only on those receivables the factor purchases. And thanks to the deep relationships it has developed with hundreds of thousands of retailers and because of its market clout, CIT is well-positioned to collect from even the most recalcitrant retailers.

“Companies of all sizes are affected by a credit loss, sometimes a smaller entity even more so,” Lal says. “Not only do you lose the amount of your accounts receivable outstanding, but you typically also lose the ongoing business with that retailer. CIT’s relationship is with both the manufacturer and the retailer, and we value both parts of that relationship.” In the case of the fitness tracker manufacturer example, CIT approved the retailer’s credit exposure involved and provided protection to the manufacturer.The manufacturer continued to operate normally, shipped and booked the sale, knowing that in the event of a default by the retailer they were protected by CIT.

With CIT’s credit protection, the company in this example was able to ship the full $5-million order to the retailer in time for Black Friday, which helped the vendor’s new division jump-start its sales. The vendor’s long relationship with the retailer was maintained, and the vendor could sleep well at night knowing that, if the retailer’s struggles continued, those credit approved sales were protected by CIT. It was a victory for all three parties — CIT had a new client relationship, the vendor successfully launched its new product, and the retailer secured its desired product for its Black Friday promotion (which in turn helped to support its turn-around plan).

CIT’s relationship is with both the vendor and the retailer, and we value both parts of that relationship.— Niraj Lal, CIT Commercial Services

CIT Commercial Services (“CIT”) is one of the nation’s leading providers of credit protection, accounts receivable management, and lending services, operating throughout the United States and internationally. CIT has been providing financing and advisory services to small, mid-sized, and large businesses for more than a century. Companies of all sizes turn to CIT for protection against bad-debt losses, to reduce days’ sales outstanding, and to enhance cash flow and liquidity. CIT’s breadth of services, experienced personnel, industry expertise, proprietary customer credit files, and comprehensive online systems are all reasons to give CIT a call. For more information: https://www.cit.com/commercial-services • 800-248-3240