NEW YORK – Car electronics sales volume generated by the nation’s top 25 car electronics retailers declined at a faster rate in 2013 than it did during each of the previous two years, but once again, their collective sales didn’t drop as much as the market as a whole, TWICE found in compiling its latest list of top dealers.

In another sign of greater industrywide weakness, only seven of the top 25 retailers posted sales gains, compared with 11 in 2012. Fourteen of the top 25 dealers posted double-digit percentage declines, and Best Buy posted the largest dollar drop of any retailer at $136 million.

The only retail channels posting dollar and share gains were consumer direct and miscellaneous (consisting of car electronics stores and automotive chains) posted sales and share gains. Mass merchants, multiregional appliance/ electronics stores, and consumer direct lost share but maintained their collective share ranks of one, two and three, respectively.

The top 25’s retail-level sales fell a collective 10.3 percent to $3.24 billion (excluding installation revenue) from 2012’s $3.61 billion. In contrast, industrywide factory-level car electronics sales fell at a faster rate of 12.3 percent to $2.45 billion, Consumer Electronics Association (CEA) statistics show.

The retailers’ collective drop followed a collective drop of 2.1 percent in 2012 and a 3.2 percent drop in 2011.

The retailers’ sales figures are based on data gathered by TWICE’s research partner, The Stevenson Company (see methodology on p. 32). The sales include car audio and video products, in-dash-navigation systems, portable navigation devices (PNDs), radar detectors, and aftermarket security/convenience systems.

CEA statistics for 2013 show a 6.3 percent drop in factory-level sales of car audio, video and installed navigation to $1.46 billion, a 24 percent drop in PND sales to $706 million, a 5.2 percent drop in car security/convenience sales to $200 million, and a 5.8 percent decline in radar-detector sales to $81 million. Total factorylevel volume fell 12.3 percent to $2.45 billion.

For its statistics, CEA estimates annual security and radar sales but tracked monthly sales of all other categories.

Industrywide sales were off not just because of continued double-digit declines in PND sales but also because of price erosion in car A/V, said consultant and former JVC Kenwood executive Keith Lehmann. “At some point, the market becomes saturated and cannot naturally consume more units, so price erosion is the main culprit to lower industry revenues,” he said.

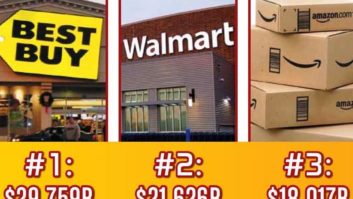

Based on Stevenson’s research, Best Buy remained No. 1 in the 2013 rankings despite a whopping 14.7 percent sales drop to $793 million. Seven other retailers posted steeper percentage drops than Best Buy, but by dint of its size, Best Buy posted the largest dollar drop at $136 million.

Industry veterans point out that Best Buy and mass merchants have scaled back their car electronics assortments in recent years. “There is no doubt that Best Buy has scaled back its head unit assortment,” said Lehmann. “This has slowly been happening for years.”

For his part, Ryan Gunter, executive director of the MESA buying group for 12-volt specialists, pointed out that so far this year, member retailers are enjoying year-over-year sales gains, in part because large retailers such as Best Buy have scaled back their assortments but also because members have become “way more promotional.”

Specialists rule: Stevenson research underscores the gains enjoyed by the mobile electronics specialist channel. Mobile electronics specialists accounted for three of the seven retailers posting sales gains in 2013. Many industry veterans would argue that four of the seven – if Crutchfield is included — are specialists.

The retailer posting the highest percentage growth in 2013 was mobile electronics specialist Audio Express (up 10.1 percent to $55 million). The next-biggest gainer was consumer-direct retailer Crutchfield, which takes a specialists’ approach to online sales. Its sales were up 9.3 percent to $109 million, followed by automotive chain AutoZone (up 6 percent to $15 million), mobile electronics specialist Mickey Shorr (up 4 percent to $18 million), Amazon (up 4 percent to $600 million), and mobile electronics specialist Car Toys (up 2.7 percent to $116 million).

Stevenson research also found continuity in the retail names qualifying for the top 25 list, with only four retailers not present in the 2012 list breaking into the 2013 list; no change in the retailers that made the top 10 in 2013; and continued concentration in sales among a small number of retailers, with the top five retailers accounting for 76.5 percent of 2013 volume and the top 10 accounting for 91 percent of volume.

The four retailers that weren’t in the 2012 rankings but broke into 2013’s top 25 are mobile electronics specialist Mickey Shorr, automotive chain Pep Boys, regional appliance/electronics retailer Electronic Express, and the Home Shopping Network. The four that dropped off this year’s list are Systemax, hhgregg, P.C. Richard & Son and Car Tunes of Allen Park, Md.

Among the top 10 retailers, Stevenson found greater stability. The retailers appearing in the 2013 and 2012 top 10 lists are identical, and all but two maintained their relative ranks compared with the previous year. Those two are Amazon and Walmart. They switched rank, with Amazon rising to two from three and Walmart falling to three from two.

The top 10 and the top five also maintained their share of sales among the top 25. The top five held a 76.5 percent share of sales, down slightly from 2012’s 77.2 percent. The top 10 grabbed 91 percent share, the same as in 2012.

The top 10 also included three of the five retailers posting percentage declines of 20 percent or more. Those three are Target with a 25 percent decline, Costco with a 21.8 percent decline, and RadioShack with a 20.6 percent. Double-digit losses were also posted by Staples, which posted the biggest drop at 27.4 percent, and QVC with a 26 percent decline.

Consumer direct, specialists: Of the two sales channels posting dollar and share gains, the consumer-direct channel led the way, thanks to dollar gains from Amazon and Crutchfield. The other four consumer-direct retailers in the top 25 posted sales declines.

Consumer-direct sales rose 2.7 percent to $776 million, boosting dollar share among the top 25 retailers to 23.9 percent, or $20 million, from 20.9 percent. Within the channel, Amazon’s car electronics sales rose by $23 million, or 4 percent, to $600 million, while Crutchfield’s sales rose $9 million, or 9.3 percent, to $109 million. The channel’s share rose to 23.9 percent from 20.9 percent.

For its part, the miscellaneous channel consisting of car electronics specialists and automotive chains posted a $10 million gain to $214 million, up 4.9 percent. The channel’s share rose to 6.6 percent from 5.7 percent.

Within the channel, two car electronics specialists – Car Toys and Audio Express – posted the highest gains, with Car Toys sales rising 2.7 percent to $116 million and Audio Express sales rising 10.1 percent to $55 million. Another car electronics specialist – Mickey Shorr – posted a 4 percent gain to $18 million. Automotive chain Auto Zone posted a 6 percent gain to $15 million, and Pep Boys posted a 2.5 percent gain to $10 million.

Shrinking channels: The channel posting the largest dollar decline was the multiregional appliance/electronics chain channel. Sales fell by $137 million to hit $830 million, down 14.2 percent, due almost completely to Best Buy’s $136 million sales decline. The only other retailer in the category was Fry’s, whose sales fell by $1 million to $36 million. The channel’s share fell to 25.6 percent from 26.8 percent.

The channel posting the second-largest dollar-sales decline was the mass-merchant channel, whose sales fell by $123 million, or 12.6 percent, to $850 million. The channel’s share fell to 26.2 percent from 26.9 percent.